Is Your Spouse Pulling Their Weight in Your Retirement Income Plan?

Turn your marriage into a tax shelter: How to legally double your exemptions and boost your monthly income.

Marriage is a partnership of love and shared life (cringy I know - but its true). But beyond the emotional bond, being married offers a distinct structural advantage when it comes to managing your wealth. If used correctly, this can serve as one of the most effective tax-saving tools in your portfolio.

I often see retired couples where one spouse holds the bulk of the investment assets while the other holds very little. While you might view this as “shared” money, this setup is a voluntary donation to the taxman.

If you are married, you have an advantage over single investors: you have two tax allowances. If you aren’t using both, you are overpaying.

Get in touch for advice on your retirement income plan: jonathan@rexsolom.co.za

The Mathematics of “Spousal Arbitrage”

South Africa uses a progressive tax system. The more you earn, the higher the percentage of tax you pay on every extra Rand. Consequently, one person earning R1 million a year pays significantly more tax than two people earning R500,000 each.

Furthermore, every individual gets specific tax “freebies” that renew annually:

Interest Exemption: R23,800 (under 65) or R34,500 (over 65) tax-free.

Capital Gains Tax (CGT): The first R40,000 of capital gain is excluded.

If one spouse holds all the assets, the second set of exemptions is wasted, and the income is pushed into a higher tax bracket.

We can solve this using Section 56(1)(b) of the Income Tax Act. This section allows spouses to donate assets to one another tax-free (no Donations Tax or Capital Gains Tax applies). This allows us to rebalance a portfolio.

The Case Study: John and Mary

Let’s look at a concrete example. John and Mary are both 65. They have built up a substantial nest egg:

R14,000,000 in a Living Annuity (Retirement Savings).

R6,000,000 in Discretionary Investments (Unit Trusts/Shares).

They withdraw an initial 5% across their portfolio in the first year of retirement.

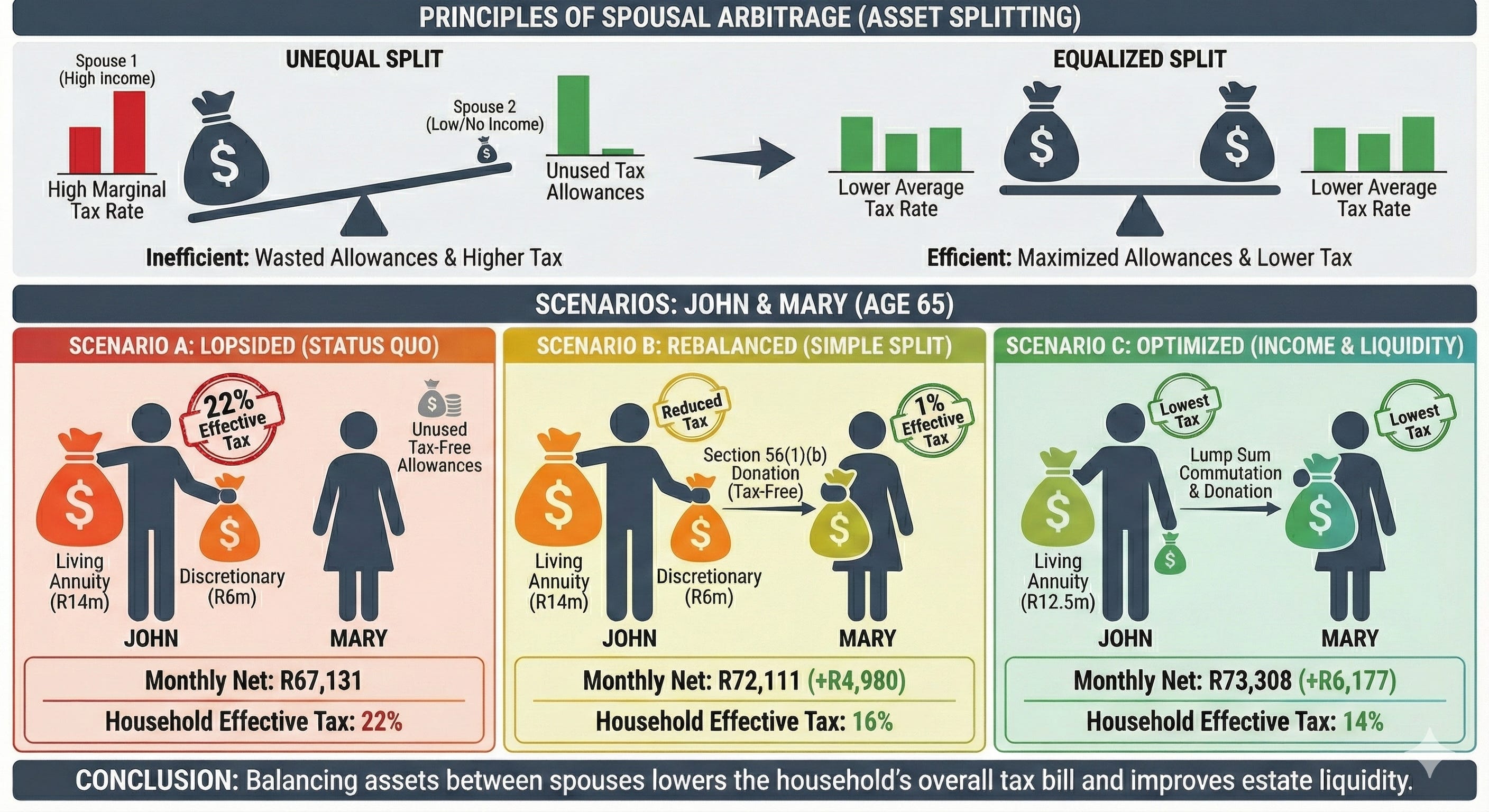

Scenario A: The Status Quo (Inefficient)

All assets are in John’s name, a common scenario where the primary breadwinner accumulated the capital. John draws income from both the Living Annuity and the Discretionary pot.

Because all the income piles up on John’s tax return, he hits a high marginal rate.

Effective Tax Rate: 22%

Total Monthly Net Income: R67,131

Scenario B: The Simple Split

We move the R6,000,000 discretionary portfolio into Mary’s name. John keeps the Living Annuity (retirement funds cannot be transferred).

Mary now utilises her interest exemption and the lower CGT brackets.

Her effective tax rate on this portion is just 1%.

John’s taxable income drops significantly.

Combined Effective Tax Rate: 16%

Total Monthly Net Income: R72,111

The Gain: An extra R4,980 per month, simply for signing a transfer form.

Scenario C: The Optimisation

We can push this further. Discretionary capital is more tax-efficient than Living Annuity income (which is taxed as pure salary). John commutes a portion of his Living Annuity (taking a lump sum) and moves that capital into Mary’s discretionary portfolio.

Living Annuity reduces to R12.5m; Discretionary increases to R7.25m (held by Mary).

This lowers the “highly taxed” income from the annuity and increases the “low tax” withdrawals from Mary’s investment.

Combined Effective Tax Rate: 14%

Total Monthly Net Income: R73,308

The Verdict

By moving from Scenario A to Scenario C, this couple increased their monthly take-home pay from R67,131 to R73,308.

That is an additional R6,177 per month (or over R74,000 per year) purely in tax savings. Over a 20-year retirement, that is nearly R1.5 million in preserved wealth, without taking any additional investment risk.

Beyond Tax: The Estate Planning Benefit

This strategy isn’t just about income; it’s about security.

In Scenario A, if John passes away, the discretionary assets fall into his estate. They may be frozen while the estate is wound up, potentially leaving Mary with liquidity issues.

By shifting assets to Mary (Scenario B and C), she has immediate access to over R7 million in liquid cash. She isn’t just a beneficiary waiting for a payout; she is an asset owner.

Conclusion

You need to view your retirement plan as a joint venture. If your spouse has unused tax allowances while you are paying a high marginal rate, you are effectively tipping SARS unnecessarily.

Review your asset split. Is your spouse pulling their weight in your tax structuring? If not, it might be time to balance the scales.

Before you go

Whenever you are ready, here are 3 ways I can help you:

Work through my “Retirement Income Blueprint”.

Create one page financial summary - I’ll send it to you with some high level feedback

Reply to this email and let’s start a conversation

My question: iwhen you move discretionary funds to another party (sell or transfer) you enact a disivestment and that attracts CGT. Have you calculated this in the total saving?