The Retirement Coin-Flip: Understanding Sequence of Returns Risk

It’s not just your average investment return that matters; the order in which you get those returns can make or break your retirement.

Summary and key takeaways

What it is: Sequence of returns risk is the danger that you will experience poor investment returns in the first few years of retirement.

Why it matters: When you are drawing an income, negative returns early on force you to sell more of your portfolio at low prices, permanently impairing your capital and its ability to recover.

The average return is misleading: Two retirees can have the exact same average return over a decade, but the one who experiences losses first can see their portfolio shrink dramatically, while the other thrives.

You can't control the sequence, but you can plan for it: Acknowledging this risk is the first step. Strategies like flexible withdrawal rates and having a proper asset allocation are key defences.

In the world of retirement planning, we spend a great deal of time talking about average investment returns. We project our financial futures based on the assumption that our portfolios will deliver a certain long-term growth rate, say 10% per year. While this is a useful exercise for accumulating wealth, it hides a danger that becomes critically important the moment you stop earning and start spending your capital: the sequence of returns risk.

Simply put, the order in which you receive your investment returns can have a more profound impact on your retirement outcome than the average return itself. A strong series of returns in your early retirement years can set you up for life, while a period of poor performance can be devastating, even if followed by a strong recovery. Understanding this is the basis on which to build a solid retirement income plan.

A Tale of Two Retirees

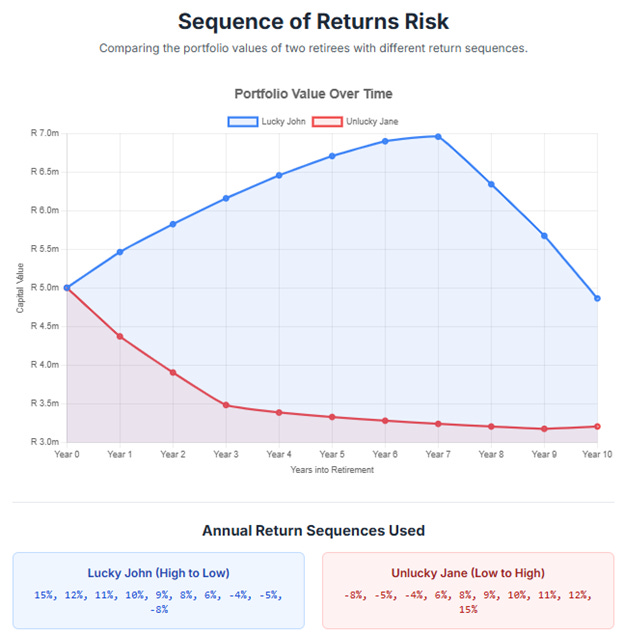

To understand this, let’s imagine two friends, Jane and John. Both retire at the same time with identical R5 million portfolios. Both decide to draw an initial income of R250,000 per year (a 5% withdrawal rate), which they will increase annually by inflation (assumed at 5% for this example). Over the next ten years, by a strange coincidence, they both achieve the exact same average annual return of 5%.

However, the sequence of their returns is a mirror image.

John’s Lucky Start: John retires just as a bull market begins. In his first three years, he gets fantastic returns of +15%, +12%, and +11%. The later years are more modest, bringing his 10-year average down to 5%.

Jane’s Unlucky Start: Jane retires at the worst possible time, right before a market downturn. Her first three years deliver returns of -8%, -5%, and -4%. The market then stages a magnificent recovery, bringing her 10-year average up to the same 5% as John.

After ten years, who is in a better position? The chart below illustrates the dramatic difference this makes to their retirement capital.

As you can see, the outcome isn't even close. Despite the identical average return, John’s portfolio is doing well. The strong early growth lifted his capital base so much that his annual withdrawals were easily covered. After a decade, his portfolio value still stands at over R4.8 million.

Jane’s situation is much worse. In those crucial first years, she was forced to sell assets at depressed prices just to fund her income. Each withdrawal took a much bigger bite out of her shrinking portfolio. Even when the market recovered, her capital base was so diminished that it could never catch up. After ten years, her portfolio has dwindled to under R3.2 million.

The sequence of returns is the coin-flip you cannot control. You don’t get to choose whether your retirement starts with an up or down market. This is why a rigid, unthinking withdrawal plan can be so dangerous. Your financial plan must be robust enough to withstand an unlucky sequence.

An optimal retirement income plan will specifically address this risk in various ways. This includes starting with a sustainable withdrawal rate, building in the flexibility to adapt your spending if markets turn against you in those fragile early years, as well as matching your income needs with assets that can reliably deliver on them.

Before you go

Whenever you are ready, here are 3 ways I can help you:

Work through my “Retirement Income Blueprint”.

Create one page financial summary - I’ll send it to you with some high level feedback

Reply to this email and let’s start a conversation